Call to Microfinance in Developed Nations

By: Red

Excerpts taken from original paper "A New Paradigm for Microfinance in Developed Nations" IJTEF Vol.9, No.1, February 2018

Microfinancing has garnered much attention from both developing countries and the United Nations in the past decade. 2005 was the United Nation General Assembly’s “Year of Microcredit” and microcredit, also otherwise called microfinancing, was recognized as a key factor in achieving the United Nation’s millennium development goal (MDG) of reducing poverty rates by 50% by 2015 [18]. Furthermore, the 2006 Nobel Peace Prize was awarded to Muhammad Yunus, creator of the Grameen Bank in Bangladesh, for the success of both idea and institution [13].

Following the rapid development of microfinancing, much research has been done on the part of both individual researchers and world organizations into the impacts that microfinancing has and could bring to developing nations. For instance, studies have concluded that microfinancing has the ability to empower both women and oppressed populations in a society through a bottom up approach [1]. These empowerments have been followed by a marked reduction in starvation, disease, and illiteracy among children, especially female, [21] and prove the necessity of microfinancing in nations who have high inequality in gender parity. However, the benefits of microfinancing isn’t limited to developing countries alone. A quick look into South Korea’s own microfinancing history and efficacy shines light to the potential for microfinancing in developed countries.

A. Microfinance in South Korea

South Korea’s official microfinancing history can be seen to have begun from August of 2007 when the dormant deposit management law was passed by Senate [20]. The law was created with the purpose of supporting microfinancing institutions and low cost insurance companies aimed towards lower and middle class citizens. Additionally, the dormant deposits would be utilized to support welfare and reduce the inequality gap between lower and upper class citizens. With the law set in place, the Dormant Deposit Management Foundation was founded later that year and changed its official name to the Central Microfinancing Foundation, and then to the People’s Financing Agency in 2016.

While microfinancing institutions have only recently been created in South Korea, the concept of microfinancing has long existed in South Korea’s traditional market system. In traditional markets, people would sometimes borrow small amounts between 10 to 50 USD from the local merchants’ association and return the money with a small interest at the end of the day or week. As a result of such systems already pre-existing in South Korea’s culture, the Central Microfinancing Foundation first worked to support the local merchants’ association and create a more sophisticated manual for microfinancing[1]. In 2011, the Central Microfinancing Foundation further decided to invest in the traditional markets and increased their number of invested traditional markets to 314 with a total of approximately 30.1 billion USD (33.8 trillion KRW) [22]. As of 2013 June, the support for microfinancing in traditional markets have expanded to over 432 traditional markets and approximately 57.2 billion dollars (64.2 trillion KRW).

Along with developments in microfinancing through traditional markets, the Central Microfinancing Foundation has also invested into its own local microfinancing branches since December 24, 2009 [23]. As of July 2017, over 160 branches have been placed nationally and support startups with up to 50 million KRW, approximately 44,568 USD, at a rate of below 4.5% yearly [17].

Besides the Central Microfinancing Foundation, South Korea has also led the world’s first government-led microfinance program through the establishment of the Smile Microcredit Bank (SMB) in December 2009; the establishment was also followed by the launch of the Sunshine Loan Program in June 2010 [12]. The program promised to provide 10 trillion KRW (or 8.45 billion USD) over the next five years for unsecured loans to low-income households through partnerships with the private sector. With the partnership of several financial institutions including the National Agricultural Cooperative Foundation, National Credit Union Federation of Korea, the Korean Foundation of Community Credit Cooperatives, and more, the program offers anywhere up to 50 million KRW for low-income households to start businesses at a ceiling interest rate of 10.6% per year [1].

B. Accomplishments and Success Factors

It is undeniable that both the government and Central Microfinancing Foundation, also called People’s Finance Agency, have made real change and progress in pioneering microfinancing in South Korea. Not only have they gained the interest of politicians and created laws supporting microfinancing (through the 2007 Dormant Deposit Management Law), but they have also managed to attract both large private-sector companies, including Samsung, Hyndai-Kia, SK, LG, POSCO, and Lotte, and major financial institutions, including Hana-Bank, Woori-Bank, Industrial Bank of Korea, and Kookmin Bank [12].

Many of South Korea’s microfinancing successes at first glance can be attributed to the support that they have been able to rally with politicians and large conglomerates. With the support, both government and Central Microfinance Foundation were able to make aggressive moves that have successfully resulted in action taking place. However, while things may be seeming bright and action may have taken place on the surface, we still must check the apple’s insides to determine whether the money and actions have resulted in real and worthwhile impact.

C. Limitations and Issues

We will first begin by analyzing the limitations of both government-led and Foundation led microfinancing models and search for the issues that each have developed as a result of environment and structure. The first limitation that the microfinancing models of South Korea face are none other than instability and reliance on current laws. Ever since the development of the Dormant Deposit Management Law in 2007, much of the funds for microfinancing have come from these dormant deposits. However, developments in both technology and law have recently posed crucial barriers that microfinance institutions must solve. Originally, bank accounts were classified as dormant deposits if the bank account owner had made no transaction with the account for the past five years. Following the classification, the bank would receive the dormant deposits and help fund microfinance institutions. However, as of August 2012, the classification between dormant deposit and active bank account has become extremely unclear with the rise in popularity of online banking. Based on a verdict from Korea’s Supreme Court, the court stated that if the bank continues to hand interest and the account holder could check this through online banking, then the account could not be classified as dormant deposit [24].

According to bank officials, banks had made compromises with the Fair Trade Commission to suggest possible changes in law regarding stopping interest after five years of no transaction. If the account was to be reactivated at a later date, the interest was to be handed all at once instead. However, due to several complications in law and interest, it seems unlikely that this suggestion will be passed. Considering that the Central Microfinancing foundation holds a total capital of 1.9 trillion KRW (or approximately 1.7 billion USD) and of this, 450 billion KRW (or approximately 401 million USD), 24%, is from dormant deposits, the reliance on law and more specifically dormant deposits, is a crucial issue that current microfinancing institutions will have to solve [24].

The second limitation that the current microfinancing model afflicts on itself is a lack of real expectations and policies. According to a microfinancing official, the Central Microfinancing Foundation helped support microfinancing for private alternative lenders under the condition that they achieved return rates of at least 95%. Considering that the average private lender’s return rate average is barely 75%, not only is 95% a ridiculous condition, but also as a result, many private lenders have completely ignored the foundation’s support [11]. Additionally, even the government’s Sunshine Loan Program held crucial flaws in expectations that had to be fixed. The Sunshine Loan Program was a part of the government’s efforts to motivate and persuade low-income families to vote during election season and consequently massive advertising was done for the product. However, there were complications inherent within the Sunshine Loan Program as they were backed by financial institutions, and if the financial institutions could not receive the money back from microfinancing, that would lead to direct losses for banks and corporations. Naturally, paperwork for the loans grew and banks became exceedingly passive and careful in their selection of loans. In fact, only 10% of the total capital was reported to have actually been lent out [9]. If the foundation and government are to truly support microfinancing and lending to low-income families, they must create policies regarding microfinancing that are realistic in expectations and allow for low-income households to truly reap the benefits.

The third crucial limitation that microfinancing places itself in the context of developed nations is in its scope of lending. The majority, if not all, microfinancing institutions currently led by the Central Microfinancing Agency and government focus foremost on helping fund start-ups for low-income households. While we can see why this may hold true in developing nations, we will go on to see why this is a limitation in the context of developed nations in the next section regarding welfare.

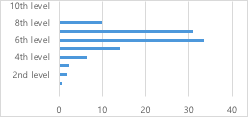

As a result of many of these limitations, issues inevitably grew especially regarding the direction and target of government and foundation-led microfinance loans. Banks became exceedingly picky about their selection of people for loans and the microfinancing loans ended up going to much of the wrong population intended. As can be seen in Fig.1, the graph represents the percentage distribution of sunshine loans handed in 2015 by credit level according to the Financial Services Commission’s 2015 September report [3]. A credit level rating of 1 is the highest possible, while a credit level rating of 10 is the lowest, just above having lost credit. When analyzing the 2015 graph, out of a total of 147,583 loans that the Sunshine program loaned out, only 193 cases were people with a credit rating of 9, and only 2 cases were people with a credit rating of 10. Considering that the two lowest credit ratings had only been able to loan out 0.13% of the total loans, the Sunshine Loan Program can be said to have failed its original purpose helping mainly low-income households. In addition, even microfinance led by the foundation wasn’t much better with a total of 15,232 loans, of which 156 were of the 9th credit rating and 31 were of the 10th credit rating, standing at 1.2% of the total loans. One of the major reasons for the low loan rate to 9th and 10th credit rating citizens from 2015 were partially due to the government’s change in policy in 2014 that decided to cover only 85% to 90% of the losses from microfinancing unlike the previous at 95% [15]. Naturally, to cover the losses, banks could only become increasingly passive and reduce the risk-taking actions of lending to those of low credit ratings.

Fig. 1. Percentage Distribution of Sunshine Loans by Credit Rating Level

D. Need For Change

It should be to no surprise that welfare systems have become increasingly difficult in developed countries recently with economy tanking. For instance, take into account Arizona where for every 100 poor families with children, only 8 families receive welfare; considering that lawmakers are reducing the maximum time amount for welfare from 5 years to just 12 months, the number can only be expected to decrease even further [19]. The situation is not much different in Pennsylvania where more than 75% of welfare applicants are denied assistance each month [4]. America as a whole, even single mothers feel the lasting effects of dropping welfare as TANF (Temporary Assistance for Needy Families), “the only cash assistance program that non-disabled, non-elderly, poor single mothers are eligible for, has dropped precipitously: It was lower in 2007 than it had been in 1970” [8].

The welfare issue is not something limited to America. Europe faces its immediate refugee crisis, and Korea too has received much criticism for its lack of welfare services [6]. As welfare reforms are leaving people behind, it becomes increasingly clear that aid for low-income households through other measures is necessary in developed countries.

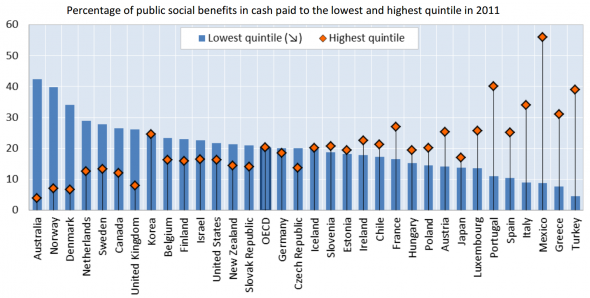

One way to alleviate this issue of welfare worldwide is to better allocate the given resources. When looking at Fig.2, data from the OECD regarding 2011 percentage of public social benefits in cash paid to the lowest and highest quintile, we begin to notice the inefficiencies present within our current welfare system [10]. While countries like Australia, Norway, and Denmark have been able to control their welfare system extremely efficiently, the OECD average points to an equal amount being handed in cash to the most financially well off 20% and worst off 20%. In other words, fixing these inefficiencies in our system could solve or cover much of the blind spots of welfare that we once had without large additional costs.

Fig. 2. Percentage of public social benefits in cash paid to the lowest and highest quintile in 2011 for OECD nations

E. Conclusion

With the decline in state of welfare internationally due to refugee crises and tanking economies, it is necessary to provide alternate aid on the side of government for low-income households. Not only can finance-welfare systems of microfinance help solve and aid allocation of welfare in forms that incentivize growing out of welfare, but it also concentrates allocation on the bottom 20% of society instead of the top 20%. Considering the existence of several policies already pre-existent that foster start-ups, a focus on welfare through a finance-welfare system of microfinance could be the solution to our welfare needs in the 21st century. It’s important for policy-makers to realize that the potential of microfinancing isn’t limited to only that of developing nations, but also to that of more developed nations if the correct modeling is done.

References

[1] Brannen, Connor. "MICROCAPITAL BRIEF: South Korean Government Launches Sunshine Microfinance Loan Program under Smile Microcredit Bank for Low-income Households." MicroCapital: On Microfinance, Mobile Money, SMEs and Other Forms of Impact Investing. MicroCapital Affairs, 2 Aug. 2010. Web. 11 July 2017.

[2] Burra, Neera, Deshmukh-Ranadive, Joy, Murthy Ranjani K., (2005). Micro-credit, Poverty and Employment: Linking the Triad, New Delhi: Sage Publications

[3] Chang, Yoonjung. "Failures of Sunshine Loan Program." Donga.com. DongA News, 22 Sept. 2015. Web. 9 July 2017.

[4] Giammarise, Kate. "Pennsylvania Denies 75 Percent of Welfare Applicants." Pittsburgh Post-Gazette. PG Publishing Company, 21 Apr. 2014. Web. 11 July 2017.

[5] Good Shepherd Microfinance. (2017). 2016 Annual Report. USA.

[6] Horn, Heather. "Can the Welfare State Survive the Refugee Crisis?" The Atlantic. Atlantic Media Company, 18 Feb. 2016. Web. 9 July 2017.

[7] Japan Times. "Making Use of Dormant Accounts." The Japan Times. Japan Times Online, 28 Jan. 2017. Web. 11 July 2017.

[8] Khazan, Olga. "How Welfare Reform Left Single Moms Behind." The Atlantic. Atlantic Media Company, 12 May 2014. Web. 13 July 2017.

[9] Kim, Chanho. An Introductory Course to Money. Seoul: Oratory and Literature Publishing, 2011. Print.

[10] Klein, Matthew C. "Welfare Spending Across the OECD." FT Alphaville. The Financial Times, 28 Nov. 2014. Web. 10 July 2017.

[11] Ko, Ilhwan. "Need to Lower Microfinance Loan Barrier." Yonhap. Yonhap News, 18 Mar. 2011. Web. 8 July 2017.

[12] Lee, Rebecca. “Smile and Sunshine: Assessing the Impact and Sustainability of Microfinance in South Korea.” SAIS. (2011): 49-60. Print.

[13] Mahjabeen, Rubana. "Microfinancing in Bangladesh: Impact on Households, Consumption and Welfare." Journal of Policy Modeling 30.6 (2008): 1083-092. Web.

[14] Microfinance Centre. Microfinance in Developed Countries. Microfinance Centre, 2010. Print.

[15] Oh, Yoonhe. “Changes in Guarantee Rate for Sunshine Loan Program.” KDI Focus..40 (2014): 1-7. Print.

[16] People Who Live Together. "2016 Financial Report for People Who Live Together." Mfk.or.kr. People Who Live Together, 29 Mar. 2017. Web. 10 July 2017.

[17] Smile Microbank. "Microfinance Loan Types and Details." Opengov Seoul. Central Microfinance Foundation, 27 Oct. 2014. Web. 10 July 2017.

[18] The United Nations. (2005). 2005 World summit outcome document. USA.

[19] Weissmann, Jordan. "How Welfare Reform Failed." Slate Magazine. The Slate Group, 01 June 2016. Web. 8 July 2017.

[20] World Daily. "Founding of the Dormant Deposit Management Foundation." Segye. Segye Ilbo, 03 July 2007. Web. 8 July 2017.

[21] Wydick, B. (1999). The effects of microenterprise lending on child schooling in Guatemala. Economic Development and Cultural Change, 47(4), 853-869

[22] Yoon, Jeehwee. "Microfinance Increases Support in Traditional Markets." Hankyung. Hankyung News, 23 Aug. 2011. Web. 8 July 2017.

[23] Yoon, Sunhee. "First Microfinance Branch Opens." Hankyung.com. Seoul Yeonhap News, 23 Dec. 2009. Web. 8 July 2017.

[24] Yoon, Yena, and Jungwun Bae. "Problems with Microfinancing and Dormant Deposit Law." Chosunbiz. Chosun, 19 June 2014. Web. 6 July 2017.

'EDITORIAL > 정보 :: Information' 카테고리의 다른 글

| Korea's #NoMarriage Movement (0) | 2019.12.04 |

|---|---|

| Living Off Campus (134) | 2019.11.22 |

| Find your cup of tea in LA (0) | 2019.11.13 |

| Top 7 Places to Eat in Koreatown, Los Angeles (0) | 2019.11.08 |

| What are you studying? (0) | 2019.11.06 |